Navigating The 2023 ‘Winter’ In Cotton Farming

⋅ BY YANGXUAN LIU ⋅

UNIVERSITY OF GEORGIA

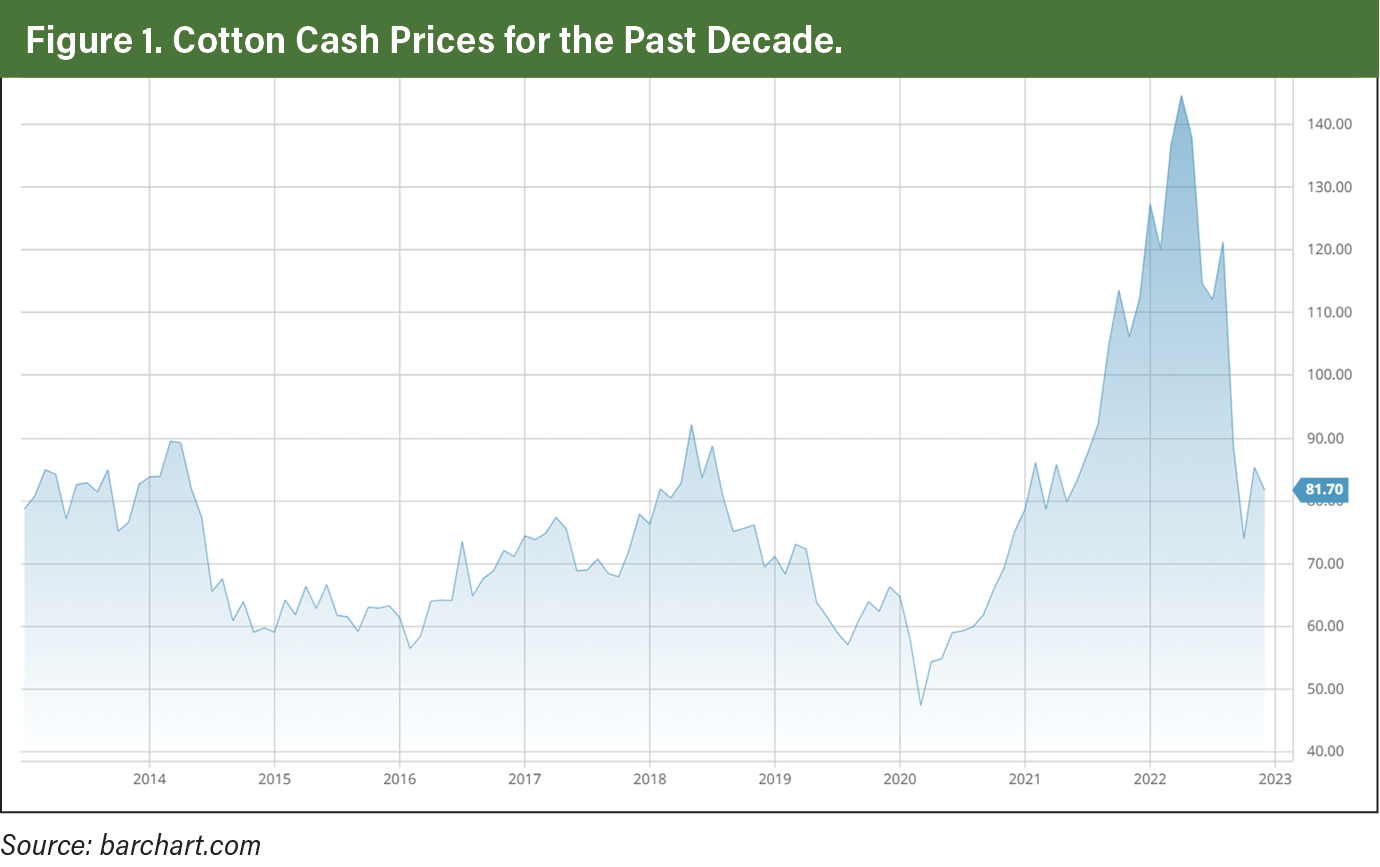

Cotton prices in the year 2022 were like a roller coaster ride, combined with an increase in volatility and the highest price achieved for the past decade (Figure 1). Multiple, rapid rallies in the cotton market were observed in 2022, followed by a quick withdrawal of speculative money. This resulted in an immediate plunge in cotton prices after the rally.

The highest cotton prices for 2022 were achieved May 4 at 149.76 cents per pound, and the lowest cotton prices in 2022 were observed Oct. 31 at 72.26 cents per pound. Several causal factors for the high cotton market volatility in 2022 include:

→ High stock market volatility.

→ Soaring inflation.

→ Supply chain disruptions.

→ Rising interest rate.

→ Appreciation of the U.S. dollar.

→ Severe drought in the Southwest United States.

Economic Slowdown, Global Cotton Demand

Looking ahead, the year 2023 could be a year of winter for cotton producers. According to the International Monetary Fund, global economic slowdown is expected in 2023 at 2.3%, combined with high inflation worldwide at 6.5%.

High inflation is depleting the personal saving rate in the United States to a historically low level, with the most recent data at 2.3%. Globally, 2022 cotton production is projected at 116.4 million bales, above the world cotton mill use at 114.9 million bales (Figure 2). The reduction in economic activity and high inflation in 2023 would likely continue to reduce consumer demand for discretionary items — such as textiles and apparel — thus suppressing cotton prices in 2023.

The cotton production profit margin would likely be lower with high input costs and low prices. On a positive note, economic recovery could probably happen during the fourth quarter of 2023, and the winter ice in the cotton market could start to melt during the cotton harvest in 2023.

U.S. Cotton Supply And Demand

In 2022, the United States planted 13.6 million acres of upland cotton, the highest in three years.

However, in 2022, the U.S. harvested only 7.7 million acres, with the overall U.S. abandonment rate for upland cotton at 43.4%, the highest on record since 1953.

Severe drought conditions hit the largest cotton production regions in the Southwest (Texas, Oklahoma and Kansas), the West (New Mexico) and Delta (Missouri). The abandonment rate for Texas reached 68%. Texas planted 7.9 million acres of cotton in 2022 — by far the largest of any state — representing 58% of total U.S. planted acres.

The November 2022 U.S. Department of Agriculture World Agricultural Supply and Demand Estimates (WASDE) report projected U.S. cotton production at 14.2 million bales for the 2022/2023 marketing year. This is slightly below the U.S. cotton demand — 12.5 million bales of exports and 2.3 million bales of domestic mill use.

In 2022, the national yield level was 856 pounds per acre. U.S. ending stocks are projected at 3 million bales in 2022. The U.S. ending stocks-to-use ratio is forecast at 20.3% for the 2022/23 marketing year.

Interest Rate, U.S. Dollar Appreciation

In response to high inflation, the Federal Reserve increased the federal funds rate to tamp inflation with its largest rate increase since the 1980s. The Federal Reserve’s commitment to bringing inflation back down to its target of 2% would likely result in a 5% or more interest rate through 2023.

The rising interest rate further accelerated the appreciation of the U.S. dollar. Cotton is a global commodity; on average, over 80% of cotton produced in the United States is exported. The appreciation of the U.S. dollar increases prices paid by foreign consumers and makes U.S. cotton less attractive.

This could result in a further decline in cotton demand from the United States and lower cotton prices for U.S. producers in 2023.

2023 Price Outlook Summary

U.S. cotton acreage and production would be likely to decline in 2023 due to lower relative price expectations with competing crops, such as peanut and corn. As this is being written on Dec. 5, 2022, December futures prices, CTZ23 (Dec ‘23), for the 2023 cotton crop are currently around 79.62 cents per pound.

The optimistic likely price for cotton in 2023 is 80 to 85 cents per pound or better, and the pessimistic likely price for 2023 is 70 to 75 cents per pound. For planning and budgeting projections, a price of 72 to 78 cents per pound is suggested for 2023.

Higher production costs and greater financial risk in 2023 make it more critical for producers to estimate and control their cost of production. Producers who are not in a marketing pool are encouraged to develop a marketing plan to protect the harvest price, as it is risky to lock in high input prices without a marketing plan for the crop.