2026 Cotton Outlook And Market Situation

YANGXUAN LIU / TIFTON, GEORGIA

TAKEAWAYS

- Cotton remains financially strained: High input costs, elevated interest rates, and weak prices have left U.S. cotton producers with ongoing negative profit margins, continuing a long-term trend of economic losses.

- Global competition and oversupply dampen prices: Rising Brazilian production, China’s diversification away from U.S. cotton, and global stocks exceeding demand have intensified market competition and kept cotton prices suppressed.

- 2026 outlook remains challenging: With cotton futures in the mid-60s, limited demand recovery, and production costs still high, growers must carefully manage expenses and adopt strong marketing strategies to reduce financial risk.

Cotton farming is an increasingly complex and financially challenging business. The 2025 production year was especially difficult for U.S. growers, as persistently high input costs, elevated interest rates, and historically low cotton prices created negative profit margins for many operations.

Cotton prices in 2025 were heavily influenced by trade policy uncertainty, particularly escalating tensions between the United States and China. At the same time, U.S. cotton faced growing competition from Brazil, which has increased production and exports while offering cotton of comparable quality at lower cost. This combination of weaker demand and heightened global competition contributed to further price pressure throughout the year.

Global Economic Slowdown and Cotton Demand

According to the October 2025 International Monetary Fund World Economic Outlook, the global economy faces ongoing turbulence tied to newly imposed tariffs and persistent geopolitical uncertainty. Growth projections have been revised downward, with worldwide expansion expected to ease from 3.3% in 2024 to 3.2% in 2025 and 3.1% in 2026. Advanced economies are forecast to grow approximately 1.5%, while emerging and developing economies are projected to see growth slightly above 4%. Rising protectionism, lingering policy uncertainty, and potential financial market adjustments continue to pose substantial risks.

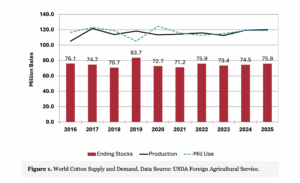

World cotton production in 2025 is projected at 120.1 million bales, exceeding global mill use, which is estimated at 118.9 million bales (Figure 1). Although consumer demand has improved somewhat over the past 2 years, production continues to outpace use, raising global ending stocks to an estimated 75.9 million bales. The buildup in global supply remains a major factor limiting any significant price recovery.

U.S. Cotton Supply and Demand

Low profitability led U.S. growers to plant only 9.3 million acres of cotton in 2025, with 7.4 million acres anticipated for harvest. Despite reduced acreage, yield performance has been strong, with a national average of 919 lb per acre, above the long-term trend, leading to an expected 14.1 million bales of production.

Demand for U.S. cotton remains historically low. At 13.9 million bales, 2025 U.S. cotton use represents the third-lowest level in the past decade, surpassed only by 2023 and 2024 at 13.6 million bales. Ending stocks are expected to increase from 4.0 to 4.3 million bales, raising the stock-to-use ratio to nearly 31%. Only 2019, a year marked by pandemic-related disruptions, exceeded this level. These conditions signal an ongoing domestic oversupply situation and further downward pressure on prices.

Long-Term Financial Struggles of Cotton Farmers

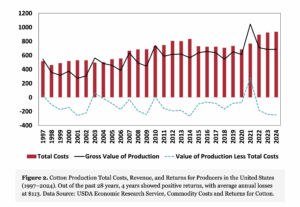

Data from the U.S. Department of Agriculture (USDA) Economic Research Service (ERS) show a long history of financial challenges for U.S. cotton producers. From 1997 to 2024, cotton exceeded total production costs in only 4 years. Across the entire period, growers faced average annual losses of $113 per acre.

In theory, commodity markets under perfect competition tend toward zero long-run economic profit, with efficiency gains needed to remain viable. However, nearly 3 decades of losses highlight a structural imbalance for cotton producers that is not sustainable without improvements in prices, productivity, or policy support.

Interest Rates and Financial Conditions

After 4 years of elevated interest rates intended to curb inflation, the Federal Reserve began easing monetary policy in late 2024. Rate cuts have progressed more slowly than expected, though, leaving producers with operating loan rates still in the 7%–8% range going into 2026. These elevated financing costs add pressure to farm profitability and increase the importance of strong liquidity and debt-management strategies.

Rising Global Competition from Brazil

The United States has historically been the world’s leading cotton exporter, sending an average of 87% of its production to foreign markets. But U.S. market share fell from 39% in 2016 to 26% in 2023 because of trade disputes and competition from Brazil. Although the U.S. share rebounded slightly to 28% in 2024 and 2025, Brazil has surpassed the United States as the world’s top cotton exporter.

Brazil’s competitive advantages are significant. Its ability to double-crop cotton, combined with higher average yields (1.8 times those of the United States from 2021 to 2024,) results in lower production costs per pound. Investment from China in Brazilian infrastructure has further strengthened Brazil’s logistical efficiency. As a result, Brazilian cotton producers continue to operate profitably, expand production, and strengthen their global market presence, while U.S. cotton producers have faced losses since 2022.

Georgia Situation

In Georgia, 840,000 acres of cotton were planted in 2025, with about 830,000 acres expected to be harvested. Production is estimated at 1.7 million bales, the lowest in 10 years. For the first time since 1993, peanut acreage has surpassed cotton acreage in the state. The contraction in cotton acreage has created challenges for associated industries such as gins, seed companies, and input suppliers. Continued declines could threaten key infrastructure that supports crop diversity. Despite reduced acreage, Georgia’s 2025 average yield is projected at 983 lb per acre, the state’s second highest in a decade.

2026 Price Outlook

Looking ahead, 2026 is expected to remain challenging for cotton production. Input costs and interest rates will likely remain elevated, and cotton prices are projected to stay weak. December 2026 cotton futures (CTZ26) are trading near 67.5 cents per pound as of December 8, 2025. Without a new trade agreement with China, demand recovery may be limited, and even with an agreement, China’s increased reliance on South American supplies will likely cap U.S. export gains.

For 2026, an optimistic price range is 69–73 cents, while a pessimistic range is 61–66 cents. A working budget range of 64–70 cents/lb is advisable. Producers not enrolled in marketing pools should implement clear pricing strategies to secure harvest prices. With production costs and financial risks remaining high, careful cost estimation and proactive marketing will be essential to maintaining farm viability. ∆

YANGXUAN LIU / UNIVERSITY OF GEORGIA

LINK: https://fieldreport.caes.uga.edu/publications/AP130-4-04/2026-cotton-outlook/