Approved by USDA’s World Agricultural Outlook Board Economic Research Service | Situation and Outlook ReportNext release isJanuary14, 2026CWS-25k|December 11, 2025

Leslie Meyer and Taylor Dew

Global 2025/26Cotton Ending Stocks Rise asProduction Remains Above Mill Use

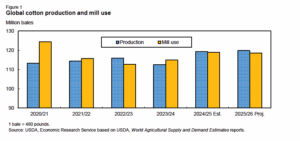

The latest U.S. Department of Agriculture (USDA) cotton projectionsfor 2025/26 (August–July) indicate that global ending stocks are forecastto rise 1.4million bales (2 percent)fromthe previous yearto 76.0million bales. The increase is a result of global production remaining above mill use for the secondconsecutive year (figure 1). China remainsthe largest holder of global stocks, accounting for 46 percentofthe globaltotal in 2025/26.

World 2025/26 cotton production is expected to increase slightlyfrom theprevious yearto 119.8 million bales, with China and Brazil the majorcontributors to the higher production.Global cotton mill use isprojected to decrease marginallyto 118.6 million bales this season, drivenbylower year-over-year use projections forChina and Turkey.Meanwhile, global cottontrade in 2025/26 is expected higher, with Brazil and the United States continuing as the primary exportersthis season while Vietnam andBangladesh are forecastas the leading importers.

Figure 1

Domestic Outlook

U.S. Cotton Crop ForecastSlightly Higherin December

USDA’sDecemberCrop Productionreport forecasts2025/26U.S. cottonproduction atnearly

14.3million bales,153,000 bales (1.1percent)abovelastmonth’s forecastbut 140,000bales (1percent)belowthe 2024/25crop.Harvested area in 2025/26is estimated at7.4million acres,compared with last season’s7.8million acres.

Growing conditionsinthe Southwest region wereimprovedrelative to the previousthreeseasons as abandonmentwas reduced considerablyfor the region.The implied U.S.abandonment rate for 2025/26 is estimated at approximately 21percent,compared with lastseason’s30percent. The 2025/26nationalyield of929pounds per harvested acre isabovethe 5-year average of 882pounds and the highestsince 2022/23’s record of953 pounds. Upland cotton production is estimated at13.9million bales, while the extra-long staple (ELS) crop isforecast at378,000 bales.(See table 10 for current production estimatesby State.)

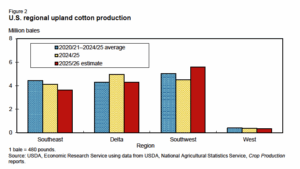

Upland cotton production thisseason isforecastlowerinthreeof the Cotton Beltregions while higherinthe Southwest(figure 2). In the Southeast, 2025/26cotton production is projected at

3.6million bales—about11.5percent(471,000 bales)below2024/25and18percentlower than the 2020/21–2024/25average. Cotton harvestedarea in 2025/26(1.7million acres)is forecastat its lowest since a similar area was harvested in 1993/94. The Southeast yield is projected well above the 5-year average (907 pounds)ata record1,036pounds per harvested acrethis season.

Cotton production in the Delta region is estimated at4.3million bales in 2025/26, 642,000 balesbelowthe year beforebutequal to the 5-year average. In 2025/26, cotton harvested areaisforecastto be1.45million acres—the lowest in a decade—whilethe region’syield is projected ata record1,423pounds per harvested acre, outperforming last season’s 1,230pounds.

Figure 2

In the Southwest, the 2025/26upland cropisprojectedat 5.6million bales,1.1 million above last season and the largest crop in 4 years as crop conditionsthis season were more favorable. While2025/26planted area (5.8million acres) wasthe lowest in a decade, harvested areaisforecastabove the 5-year average and the highest since 2021/22. Harvested acreagein the Southwest isprojectedat4.0million acresin 2025/26—with acalculatedabandonmentrate of32percent, compared with last season’s 50percent. The 2025/26Southwestupland yieldisforecastat679pounds per harvested acre,marginally above the5-year average.

In the West,2025/26upland productionis projected at335,000 bales,18percent belowthe 5-year average andthe second-lowest production totalsince 1932/33. Harvested area is estimated at a relatively low 127,000 acres, while this season’syield (1,269pounds perharvested acre) is forecastnear the 3-year average. Theextra-long staple (ELS)crop—grownmainly in the West—is projected at378,000 bales in 2025/26, belowlast season’s471,000bales.Withharvested area estimatednear recent lows,the ELS yield (1,303pounds perharvested acre) is forecastto beits highest in 5 years.

U.S. Cotton Demand Estimate Reduced; StocksHigher

U.S. cotton demand for 2025/26is projected slightly lowerin Decemberat 13.8million bales,above the previous 2 years’ level of 13.6million bales.U.S. cotton exports accountfor thelargest shareof demandand are forecast at 12.2million bales in 2025/26. U.S.mill useisexpected tocontinue itstrend lower and accountsforan additional1.6million balesthis season—the lowest innearly150 years.

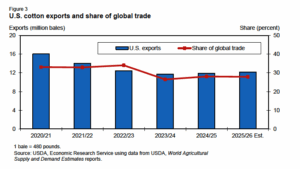

With a modest rise in theworld tradeprojectionthis season—including higher import demand from countries such as Vietnam, China, and Turkey—higher U.S.cotton export prospects areexpected despite increased competition from Brazil.Based on theDecemberprojections, the2025/26U.S. shareofglobaltradeis forecastto remain relativelystablethis seasonatabout28percent, compared with the 2020/21–2022/23 average of 33percent(figure 3).

Figure 3

With the December increase in the U.S. cotton production estimate and demand reduced slightly, 2025/26 U.S. ending stocks are forecast 200,000 bales higher this month, at 4.5 million bales. U.S. cotton stocks are 500,000 bales above 2024/25 and 1.35 million bales above 2023/24. The stocks-to-use ratio (32.6 percent) is forecast above 2024/25’s 29 percent and the highest since 2019/20. Based on the U.S. and world cotton supply and demand estimates and recent prices, the 2025/26 average U.S. upland cotton farm price is forecast at 60 cents per pound, compared with the final 2024/25 price of 63 cents per pound and 2023/24’s 76.1 cents.

International Outlook

Global2025/26Cotton Production ForecastSlightly Higher

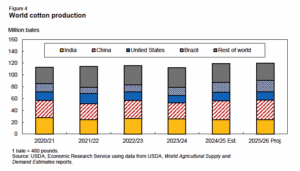

Global cotton production in 2025/26 is projected at 119.8 million bales,revised slightly lowerfrom November and now510,000 bales(0.4 percent)above the previousyear. For 2025/26,cotton production prospectsformost of themajor-producing countries are split, withyear-over-yeardeclines in Australia and the United States projected to partially offsetthe increasesin China and Brazil(figure 4). India and Pakistan remain unchanged in 2025/26 fromthe previousyear. World 2025/26 cotton harvested areais forecast at 29.4 million hectares(72.8 million acres), nearly 2.5 percent belowthe previous year.The 2025/26 global cotton yield is forecastto be 886 kilograms(kg)per hectare (790 pounds per acre), 10 percent above the 5-yearaverage and the highest on record.

World cotton production remainsconcentratedamong a few countries, with the top fourcountries (China, India,Brazil, and the United States) accounting for 76 percent of totalexpected production in 2025/26, 2.3 percentagepoints above the previousseason. China andIndia are expected to continue asthe leading cotton producers in 2025/26, accounting for 28percent and 20 percent,respectively, ofthe global total.

China is projected to produce 33.5 million bales of cotton, up 1.5 million bales (5 percent) from2024/25 anditslargest crop since 2012/13.China’s harvested area is expected to increase 5percent in 2025/26 to nearly 3.1million hectares.The higher harvested area more than offsets a small (0.4 percent) decline in expected yield to 2,391 kg per hectare, still the second highest onrecord. Production in India is forecast at 24.0 million bales, unchanged from 2024/25, with anincrease in yield offsetting a decrease in harvested area.India’s yield is projected 3 percenthigher at 467 kg per hectare, while harvested area is projected to decline 300,000 hectaresfrom last seasonto 11.2million hectares.

Figure 4

Brazil’s production is estimated to rise 10 percentfromthe previous yearto a record 18.75million bales. The growth is aresult of a nearly 8-percent (150,000 hectare) increase in harvested areato 2.1 million hectares and a 2-percent increase in yield. Brazil’s yield isforecastto bethe highest on record at1,944 kgper hectare thisseason, compared with 1,903 kg perhectare realized in 2024/25 and the previousrecord of1,911 kg per hectare in 2023/24.

In 2025/26, cotton production in Pakistan isexpected to remain unchanged from 2024/25 at 5.0 million bales. Harvested area in Pakistan is expected to decrease2.5percent (50,000hectares)to 1.95 million hectares in 2025/26, offset by an increase in yield thatresults in the unchangedproduction total. Yield isexpected to increase 14 kg per hectare in 2025/26 to 558 kg perhectare. Australia’s cotton area and productionareexpected to decrease 20 percenteach to 480,000 hectares and 4.5 million bales,respectively,due to lessfavorable growing conditionsin2025/26. Australia’s national yield, however,is forecast to riseslightlyto 2,041 kg per hectare.

WorldCotton Mill Use ProjectedSlightly Lowerin 2025/26

Globalcotton mill usein 2025/26is forecastto decrease marginally(0.3 percent)from the yearbefore to118.6million bales. Although the worldcottonuse projection is 3 million bales above the most recent4-year average,itremainsapproximately 5percent below the record (124.5million bales)set in 2020/21. Global economic uncertainties and favorable syntheticfiber pricesin recent yearshave weighed on cottonmill use.

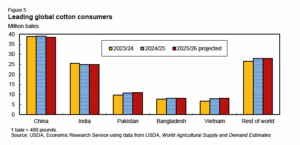

For 2025/26, cottonmill use estimatesare mixed for the leading cotton-spinning countries—China,India, Pakistan, Bangladesh, and Vietnam—with China expected to see the largestreduction thisseason (figure 5).Despite a500,000-bale lowerforecastfor China in 2025/26, the top fivecountriesareexpected to account forapproximately 76.5 percentof totalglobalcottonmill use, similarto last season.

Figure 5

For China, 2025/26 cotton mill use is forecast at 38.5 million bales, a 1.3-percent reduction from the previous year but equal to the 3-year average. Despite the year-to-year reduction, China will remain the leading cotton spinner in 2025/26, contributing nearly one-third of the global total.

For India—the second-largest cotton spinner—2025/26 mill use isforecast at 25.0million bales,unchanged from both the Novemberforecast and the previous year. India is expected to accountfor 21 percent of global mill use this season.

Cotton mill use is forecastto increase in Pakistanand Vietnamin 2025/26,contributinga combined 16percent ofworld mill use,similar tothe previous year. In Pakistan, 2025/26cotton mill use isexpected to increase nearly 1 percentafter last season’s 11-percent gain.Cotton mill use in Pakistanis forecastto reach10.9million balesthis season,matching its highest levelsince 2008/09.Mill use inVietnamis forecasttocontinue its trend higher, reaching a record 8.1million bales in 2025/26. Cotton mill use in Bangladesh is also forecast at 8.1 million bales but is100,000 bales lowerthan a year ago and belowthe 2021/22 record of 8.8 million bales.

GlobalCotton Trade and Stocks Higherin 2025/26

Worldcotton trade in2025/26is projectedto expand,largelythe result ofincreased importprojectionsfor several major importers. Global imports are forecastat 43.7million bales in2025/26, slightly above the 5-year average.Vietnam and Bangladesh are forecastto be the leading cotton importersin 2025/26.Cotton importsby Vietnamareexpected to reach a record 8.1 million bales in 2025/26 to help supply its growing textile industry.Imports by Bangladesh(at 8.0 million bales)areexpected to remainsimilar tolastyearalthough the level is belowthe 8.45-million-bale record in2021/22.Cotton imports by Pakistan and China are forecastat 5.9 million bales (down200,000 balesfrom last year) and 5.4 million bales (up about200,000bales), respectively.

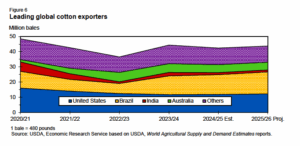

Global cotton exportsare forecasthigherin 2025/26, withBrazil and the United Statesaccounting for the growth (figure 6). For Brazil, cotton exports are expected to benefit fromanother record crop as exportable supplies rise 2.3 million bales. Brazil isprojected to exporta record14.5 million balesin 2025/26, up 11 percent(1.5 million bales)froma year ago.Brazil isalso expectedto be the largest exporter for thethirdconsecutive seasonwith itsshare of2025/26global cotton trade forecast near 33percent.Slightly higher exportsby the UnitedStates(up 300,000 bales or 2.5 percent)arealso the result of increased supplies ofhigh-qualitycotton.Slight offsetting declines are seen forAustralia, India, andMali while exports by Benin are expected unchanged from 2024/25.

Figure 6

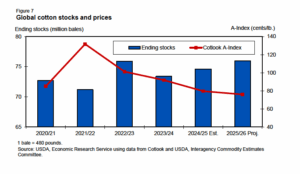

Based on the latest cotton supply and demand projections,globalending stocks are fore castat 76.0million bales in 2025/26, compared with 74.6million baleslast season.World cotton stocks are forecast toincreasenearly2 percent (1.4million bales) as global production exceed smilluse once again this season.

For most of the majorproducing countries, 2025/26cotton endingstocksare forecastto rise, with the exception of Australia where a smaller crop is reducing supplies.Cotton stocks in China—the largest holder of cotton—are forecastat 35.2 million bales, up nearly 1 percentfrom last year. At the end of 2025/26, China is expected to hold 46 percent of global cotton stocks.In India,this season’s cotton stocks are projected at 10.5 million bales(14 percent of the globaltotal), or500,000 bales (5 percent) higherthan last year. Significant increases are also seenforthe United States andBrazil, whichare expected to account fora combined 11.5 percent oftheworld cotton stocks in 2025/26.U.S. stocks are forecast to increase12.5 percent(500,000 bales)to 4.5million bales in 2025/26.Cotton stocks in Brazil are projected atnearly4.3millionbales in 2025/26, a year-over-year increase of25percent(850,000 bales)due to a record crop.

With continued economic uncertainty affecting world cotton demand for textile and apparel products, global cotton stocks and the stocks-to-use ratio (64 percent) are projected slightly higher in 2025/26. Consequently, the 2025/26 world cotton price (Cotlook A-Index) is expected to decline for the fourth consecutive season, averaging below the 2024/25 level of 80 cents per pound (figure 7).

Note: The information in this report reflects data available at the time of publication of the December 9, 2025, World Agricultural Supply and Demand Estimates (WASDE) report, unless otherwise specified.

Suggested Citation

Meyer, L., & Dew, T. (2025). Cotton and wool outlook: December 2025 (Report No. CWS-25k). U.S. Department of Agriculture, Economic Research Service.

LINK: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://ers.usda.gov/sites/default/files/_laserfiche/outlooks/113563/CWS-25k.pdf?v=82408